Companies Act, 2013

Procedure for Initial Public Offer on SME Board

Priya Gandhi

Priya Gandhi

Introduction

An Initial Public Offering (IPO) allows a privately held company to raise capital by offering shares to the public and becoming a publicly listed entity. For Small and Medium Enterprises (SMEs), listing on platforms like BSE SME or NSE Emerge offers access to funding, visibility, and growth opportunities.

Before filing the offer document with SEBI and the stock exchange, a private company must convert into an unlisted public company. The IPO process involves regulatory approvals, detailed disclosures, and compliance checks by SEBI and the stock exchanges.

While an IPO offers significant benefits, it also brings added regulatory responsibilities. This document outlines the key steps and requirements for SMEs planning to go public on the SME Board.

Conditions prohibiting public offer:

- If Issuer/promoters/directors/selling shareholders are debarred by SEBI from accessing capital markets

- If any of such promoters or directors are involved in other SEBI debarred company

- If the issuer or any of its promoters or directors is a wilful defaulter or a fraudulent borrower or a fugitive economic offender

- Presence of any outstanding convertible securities or any other rights to receive equity shares of the issue.

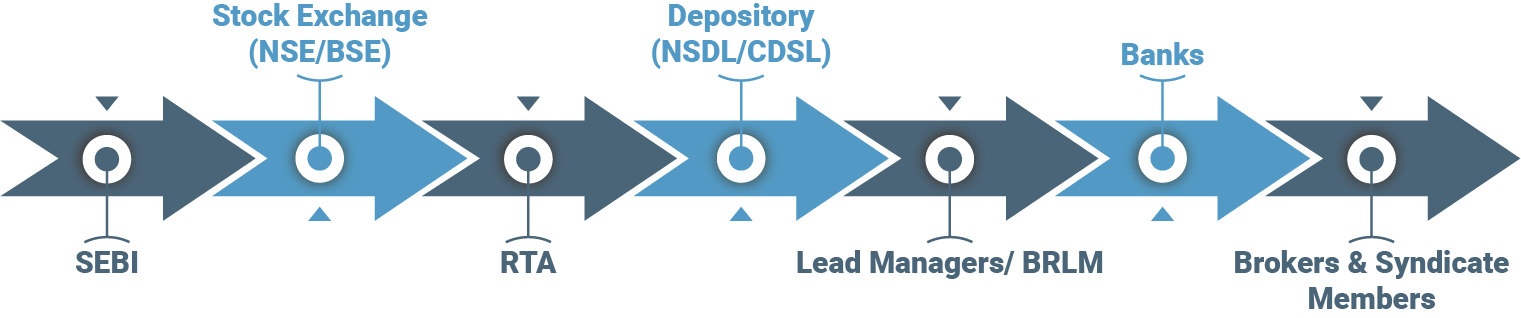

Intermediaries involved in the IPO

Applicable Provisions

- Section 23, 26, 32, 39, 40, 62, 96, 100, 173 of Companies Act, 2013

- Rule 12 of Companies (Prospectus and Allotment of Securities) Rules, 2014

- Regulation 228, 229, 230, 236, 237, 238, 239, 241, 244, 245, 246, 247, 248, 249, 250, 251, 252, 253, 254, 255, 256, 257, 258, 259, 260, 261, 262, 263, 264, 265, 266, 267, 268 of SEBI (ICDR) Regulations, 2018

Mandatory Requirements

-

Issuer Company intending to make public offer shall have

- Post-issue paid-up capital is less than or equal to Rs. 10 crore

- Issuer with post-issue paid-up capital between Rs. 10 crore and Rs. 25 crore may also issue specified securities under Chapter IX – Initial Public Offer by Small and Medium Enterprises

- Satisfy the track record and/or other eligibility conditions of the SME Exchange where its securities are proposed to be listed

-

Other General conditions

- Have minimum operating profits (EBIDTA) of Rs. 1 crore from operations in at least two of the last three financial years.

- All its specified securities held by the promoters are in dematerialised form prior to filing of the offer document.

- All its existing partly paid-up equity shares have either been fully paid-up or have been forfeited.

- Have verifiable firm financial arrangements for ≥ 75% of project funding, excluding proposed issue and identifiable internal accruals.

- Offer for sale by selling shareholders must not exceed 20% of the total issue size and shares offered for sale must not exceed 50% of their pre-issue fully diluted shareholding.

- Issue proceeds cannot be used to repay loans taken from promoters, promoter group, or any related parties, either directly or indirectly.

- Amount allocated for general corporate purposes in the offer document should not exceed 15% of the amount being raised or ₹10 crore, whichever is lower and the combined amount for general corporate purposes and objects where no acquisition or investment target is identified should not exceed 35% of the amount being raised.

- Promoters shall hold at least 20% of the post-issue capital and minimum promoters’ contribution is locked in for 3 years from commercial production start or IPO allotment, whichever is later.

- Entire pre-issue non-promoter shareholding locked-in for 1 year from IPO allotment date.

- If the issuer was previously a partnership firm or LLP, the track record of operating profit will be considered only if the financial statements:

- Are revised in the format prescribed under the Companies Act, 2013

- Make adequate disclosures as required by Schedule III of the Companies Act, 2013

- Are certified by peer-reviewed auditors stating compliance with Schedule III and accounting standards.

- If the issuer is formed due to a merger or division of a company, the track record will be considered only if the financial statements meet the same requirements as above.

- Within this 35%, the amount allocated for objects without identified acquisition or investment targets should not exceed 25% of the amount being raised.

- Promoters’ holding exceeding the minimum contribution will be locked-in as follows:

- 50% of the excess holding locked in for 2 years from the IPO allotment date

- The remaining 50% locked in for 1 year from the IPO allotment date.

- Certificates of locked-in specified securities must be marked “non-transferable” with the lock-in period noted, and if dematerialized, the lock-in must be recorded by the depository.

Procedure to be followed

-

Convene a Meeting of Board of Directors

Company shall convene a Meeting of its Board of Directors to pass a Board resolution for the following:- To consider and approve the public offer subject to Members’ Approval of the Company

- To consider conversion into a public company (Applicable, in case of Private limited company)/ in-principal approval for going public, including that of alterations in articles of association (AoA) and memorandum of association (MoA), if required.

- To delegate authority to Company Secretary or any one director of the company to sign, certify and file the required form with Registrar of Companies and to do all such acts and deeds as may be necessary to give effect to issue such public offer.

[Please refer to the Procedure for Conducting Board Meeting for further details.]

-

Convene General Meeting

Company shall pass special resolution for bringing public offer, in a duly convened meeting of its members.

[Please Refer the Procedure for Preparation and Signing of Minutes of General Meeting.] -

File Form MGT-14 with ROC

Company shall file a copy of Board Resolution and Special Resolution passed in its duly convened Board meeting and General meeting in Form MGT-14 within 30 days of passing such resolution along with the requisite documents and fees, with the Registrar of Companies (ROC). -

Appointment of Lead Managers, Other Intermediaries and Compliance Officers

Issuing company shall make following appointments for the purposes of bringing Initial Public Offer (IPO):- One or more Merchant Bankers which are registered with the Board as lead manager(s) to the issue

- Merchant bankers or stock brokers, registered with the Board, to act as underwriters

- Other SEBI-registered intermediaries may be appointed after lead manager independently assesses their capability to fulfil obligations

- Syndicate member(s) (In case of IPO) and bankers to issue (In case of any other issue)

- Registrar to the issue which is registered with the Board, and has connectivity with all the depositories

- Qualified Company Secretary appointed as Compliance Officer.

-

Enter into Agreement with Intermediaries and Underwriting Requirements

- Issuing Company shall enter into agreement with:

- Depository for dematerialization of the specified securities already issued and proposed to be issued

- Lead manager(s) in the format specified in Schedule II and with other intermediaries as required under the respective regulations applicable to the intermediary concerned

- Lead manager(s) may enter into an agreement with nominated investors specifying the number of securities they agree to subscribe at the issue price in the event of under-subscription

- Underwriting requirements are as under:

- IPO must be 100% underwritten, with lead managers underwriting at least 15% themselves

- Issuer and lead managers appoint registered underwriters and may include nominated investors for unsubscribed shares

- Lead managers must file a declaration with SEBI confirming full underwriting and details of all underwriters before the issue opens

- If underwriters or nominated investors don’t fulfill their commitments, lead managers must cover the shortfall

- All underwriting arrangements must be disclosed in the offer document.

- Issuing Company shall enter into agreement with:

-

Filing of Draft Offer Document

-

Submission to SEBI:

- File the draft offer document through the lead manager(s), along with the applicable fees as specified in Schedule III (Fees to be Paid) of the ICDR Regulations.

- These documents should also be furnished in soft copy as well.

-

Submission to SME Exchanges:

- File draft offer document with the SME Exchange(s) where the specified securities are proposed to be listed, along with Due Diligence Certificate (Form A of Schedule V), Site Visit Report of the issuer, and Additional Confirmations (Form G of Schedule V).

- If the issuer was previously a proprietorship, partnership, or LLP, it must have been in existence as a company for at least one full financial year before filing the draft offer document.

- If there is a complete change of promoters, or if new promoters acquire more than 50% of shareholding, the issuer can file a draft offer document only after one year from the date of such change.

Note:

-

Submission to SEBI:

-

Public Availability and Communication of Draft Offer Document

-

Public Comments on Draft Offer Document

Make the draft offer document filed with SEBI available for public comments for a period of at least 21 days from the filing date, which can be achieved by hosting the document on the websites of:- SEBI

- Stock exchanges where the specified securities are proposed to be listed

- Lead manager(s) associated with the issue.

-

Public Announcement

Within 2 days of filing the draft offer document with SEBI, the issuing company must make a public announcement in:- One English national daily newspaper with wide circulation

- One Hindi national daily newspaper with wide circulation

-

Public Comments on Draft Offer Document

-

Filing Updated Draft Offer Document

- After considering public comments and incorporating necessary changes, the issuing company must file an updated draft offer document with SEBI through the lead manager(s), highlighting all changes made, before filing the offer document with the Registrar of Companies (ROC).

- Such updated draft offer document should also be filed with the SME Exchanges.

-

File Red Herring Prospectus with ROC

File the red herring prospectus in Form GNL-2 with the Registrar, at least 3 days prior to the opening of the subscription list and the offer.

Note:- Any variation between the red herring prospectus and the final prospectus shall be highlighted as variations in the prospectus.

- Price may be determined at a later date before filing the prospectus with the ROC, wherein:

- Issue price or a price band must be mentioned in the offer document (In case of Fixed Price Issue)

- Floor price or a price band must be mentioned in the red herring prospectus (In case of Book Built Issue). If the floor price or price band is not disclosed in the red herring prospectus, then the issuing company must announce it at least 2 working days prior to the opening of issue, in the same newspapers in which the pre-issue advertisement was released or together with such pre-issue advertisement.

-

Filing of Offer Document with SEBI and SME Exchange

- File a copy of the final offer document with SEBI and the SME Exchange(s) through the lead manager(s), after filing the offer document with the ROC.

- In case of any change(s) in the final offer document concerning matters specified in Schedule XVI of the ICDR Regulations, an updated offer document must be filed with SEBI along with the applicable fees as specified in Schedule III.

-

Issue-Related Advertisements

- Issuer after filing the prospectus must publish a pre-issue and price band advertisement in the same newspapers where the public announcement was made, following the specified format.

- Advertisements for issue opening and closing can be published in prescribed formats, but no ads should claim full or oversubscription while the issue is open.

- The issue closing announcement can only be made after at least 90% subscription is confirmed by the lead manager and certified by the registrar, and not before the closing date (except the official closing ad).

-

Obtain In-Principal Listing Approval from the SME Exchanges

Company shall make an application to one or more SME Exchanges for the listing of its specified securities on such SME Exchanges, to obtain in-principal approval and choose one of them as the designated stock exchange. -

Allocation and Allotment of Securities

-

Minimum Offer to Public:

For an IPO, at least 25% of each class or kind of equity shares or debentures convertible into equity shares issued by the company must be offered and allotted to the public in terms of the offer document. -

Opening of the Issue:

Issue must be opened within 12 months from the date of issuance of observations by SEBI and/or be opened after at least 3 working days from the date of filing the prospectus with the ROC. Issue shall not be open for more than 10 working days. -

Application Process:

Every application form related to the issue must be accompanied by a copy of the abridged prospectus and bids should be accepted only using the Application Supported by Blocked Amount (ASBA) facility. -

Allocation of Securities:

- Allocation in the net offer category shall be as follows:

- At least 35% to retail individual investors

- At least 15% to non-institutional investors

- Remaining 50% to qualified institutional buyers, with at least 5% of this portion allocated to mutual funds.

- Allocation for Non-Institutional Investors (NIIs) in Book Building Issue shall be as follows:

- 1/3rd of the NII portion is reserved for applicants applying for more than two lots, up to Rs. 10 lakhs

- 2/3rd of the NII portion is reserved for applicants applying for more than Rs. 10 lakhs.

- Allocation in the net offer category shall be as follows:

-

Other Requirements:

- Obtain grading for the IPO from one or more CRA registered with SEBI.

- Abstain from releasing any advertisement that gives an impression that the issue has been fully subscribed or oversubscribed or indicating investor’s response to the issue.

- Ensure that the specified securities are allotted and/or application monies are refunded or unblocked within the timelines specified by SEBI.

- Report transactions in securities by promoters and promoter group during the period between the filing date of the draft offer document or offer document and the closure date of the issue, to the stock exchange(s) within 24 hours of such transactions.

- Any proposed pre-IPO placement disclosed in the draft offer document must be reported to the stock exchange(s), within 24 hours of such pre-IPO transactions (in part or in entirety).

Note: If the issue is made through book building process, allocation shall be as under:

- At least 10% to retail individual investors

- At least 15% to non-institutional investors

- At least 75% to qualified institutional buyers, with at least 5% of this portion allocated to mutual funds.

-

Minimum Offer to Public:

-

Obtain Listing and Trading Approval from Stock Exchange

Issuer shall obtain listing and trading approval from SME Exchanges and commence trading of the securities (mandatory listing within 3 days of issue closure date). -

Filing Form PAS-3 with the Registrar

File return of allotment in Form PAS-3, within 30 days of passing of the resolution for allotment of shares with following attachments:- Copy of special resolution passed in the general meeting of the company

- Copy of Board Resolution for Allotment of Shares

- List of Allottees stating their names, addresses, occupation and number securities allotted to each of allottees

- Valuation Report of Registered Valuer

- PAS-5 (Record of allottees) within 15 days from the date of allotment

- Any other mandatory attachment if necessary.

-

Filing of the Form CRF with the respective ROC

Issuer shall file Form CRF with the respective ROC, for change of the CIN number of the company from “U” to “L”. -

Post Issue Compliances

-

Post-Issue Advertisements:

- Lead manager(s) must ensure that an advertisement is released within 10 days from the completion of various activities, providing details such as:

- Subscription details

- Basis of allotment

- Number, value, and percentage of all applications, including ASBA

- Number, value, and percentage of successful allottees

- Date of completion of dispatch of refund orders or instructions to self-certified syndicate banks by the registrar

- Date of credit of specified securities

- Date of filing of listing application

-

This advertisement must be published in:

- At least one English national daily newspaper with wide circulation

- At least one Hindi national daily newspaper with wide circulation

- At least one regional language daily newspaper with wide circulation at the place where the registered office of the issuer is situated

- Additionally, the details specified above must also be placed on the websites of the stock exchange(s).

- Lead manager(s) must ensure that an advertisement is released within 10 days from the completion of various activities, providing details such as:

-

Final Post-Issue Report:

Lead manager(s) must submit a final post-issue report in the format specified in Part A of Schedule XVII (Formats of Post Issue Reports) of the ICDR Regulations, including a due diligence certificate as per Form F of Schedule V (Formats of Due Diligence Certificates), within:- Seven days of the finalization of the basis of allotment or

- Seven days of refund of money in case of failure of the issue.

-

Market Making Requirements:

- Lead managers must ensure compulsory market making on the SME Exchange for at least 3 years after listing.

- Market makers can work with nominated investors for market making, with SME exchange approval.

- Market makers must keep an inventory of at least 5% of the listed securities.

- Market makers cannot buy shares from promoters or promoter-related persons during the market making period.

- Promoters’ shares aren’t eligible for market making unless unlocked and approved by the SME Exchange.

-

Continuous Disclosure Requirements:

Issuing company must comply with continuous disclosure requirements as specified by SEBI, which includes reporting any material developments or changes that may affect the investors’ decision-making process, and also, ensure that all information disclosed is accurate, timely, and in accordance with SEBI’s guidelines.

-

Post-Issue Advertisements:

Abbreviation used

- IPO – Initial Public Offering

- SEBI – Securities and Exchange Board of India

- NSDL – National Securities and Depositories Limited

- CDSL – Central Depository Securities Limited

- ROC – Registrar of Companies

- BRLM – Book Running Lead Managers

- CIN – Corporate Identification Number

- ICDR Regulations – Securities and Exchange Board of India (Issue of Capital and Disclosure Requirements) Regulations, 2018

- BSE – BSE Limited

- NSE – National Stock Exchange of India Limited

- CRA – Credit Rating Agency

- AoA – Articles of Association

- MoA – Memorandum of Association

Tell us how helpful was this post?

Our Solutions

Related Procedures

- Conversion of Debt or Loan into Securities (Listed Company)

- Procedure for Intimating Satisfaction of Charge (Within 300 Days)

- Procedure for Change in Liability Clause of Memorandum of Association (MOA)

- Procedure for Conversion of Section 8 Company into any Other Kind

- Procedure for Appointment of Women Director on Board

- Procedure for Making Calls on Shares

- Procedure for Sale of the Whole or Substantially the Whole of Undertaking of the Company

- Procedure for Claiming Unpaid Amounts and Shares from IEPF

- Procedure for Contribution to Bona fide and Charitable Funds etc.

- Procedure for Preparation and Signing of Minutes of Board/Committee Meeting