Introduction to Climate-Related Disclosures

Climate-related disclosures are simply a way for Organisations to disclose how climate change affects their business and how their activities impact the environment, as climate risks like extreme weather, rising temperatures, and stricter environmental regulations become more common, businesses are expected to share this information with Investors, Regulators, and Public.

Why Climate Disclosure Requirements Are Increasing Worldwide?

Climate related changes are no longer an environmental issue they have become a financial issue, also a key part of sustainability reporting and help organizations to explain how climate change affects their operations, what risks they face, what opportunities they see, and how much they contribute to emissions and how “climate-ready” an organisation is.

Different parts of the world approach these disclosures in slightly different ways; hence, two leading frameworks guide these disclosures:

Global The IFRS S2 Climate-Related Disclosures

U.S. The Enhancement and Standardization of Climate-Related Disclosures for Investors

Overview of Global Climate Disclosure Frameworks

IFRS S2 Climate-Related Disclosures of the International Sustainability Standards Board, establishes a global baseline for climate-related disclosures and mandates the reporting on emissions.

What is the Objective of IFRS S2?

The primary objective is to provide the investors useful, decision-ready information and entities are expected to disclose climate-related risks and opportunities that could impact:

What does IFRS S2 cover?

It looks at both sides of the climate equation:

- Climate Risks: Either Physical or Transition

- Climate related Opportunities.

What needs to be disclosed under IFRS S2?

Entities shall disclose the following information:

- Who is responsible to oversees climate-related risks and opportunities.

- How management process, controls, monitor, manage and oversee climate-related risks and opportunities.

- Current and expected effects on business model and value chain.

- Carbon footprint, including its value chain.

- How climate related risks and opportunities shape the strategy and decision-making.

- How they Impacts on financial position and long-term plans.

- How resilient the business is under different climate scenarios and how they respond to climate changes, developments, and uncertainties.

Companies are required to disclose relevant information as comparative information, except for the first annual reporting period in which it applies this Standard.

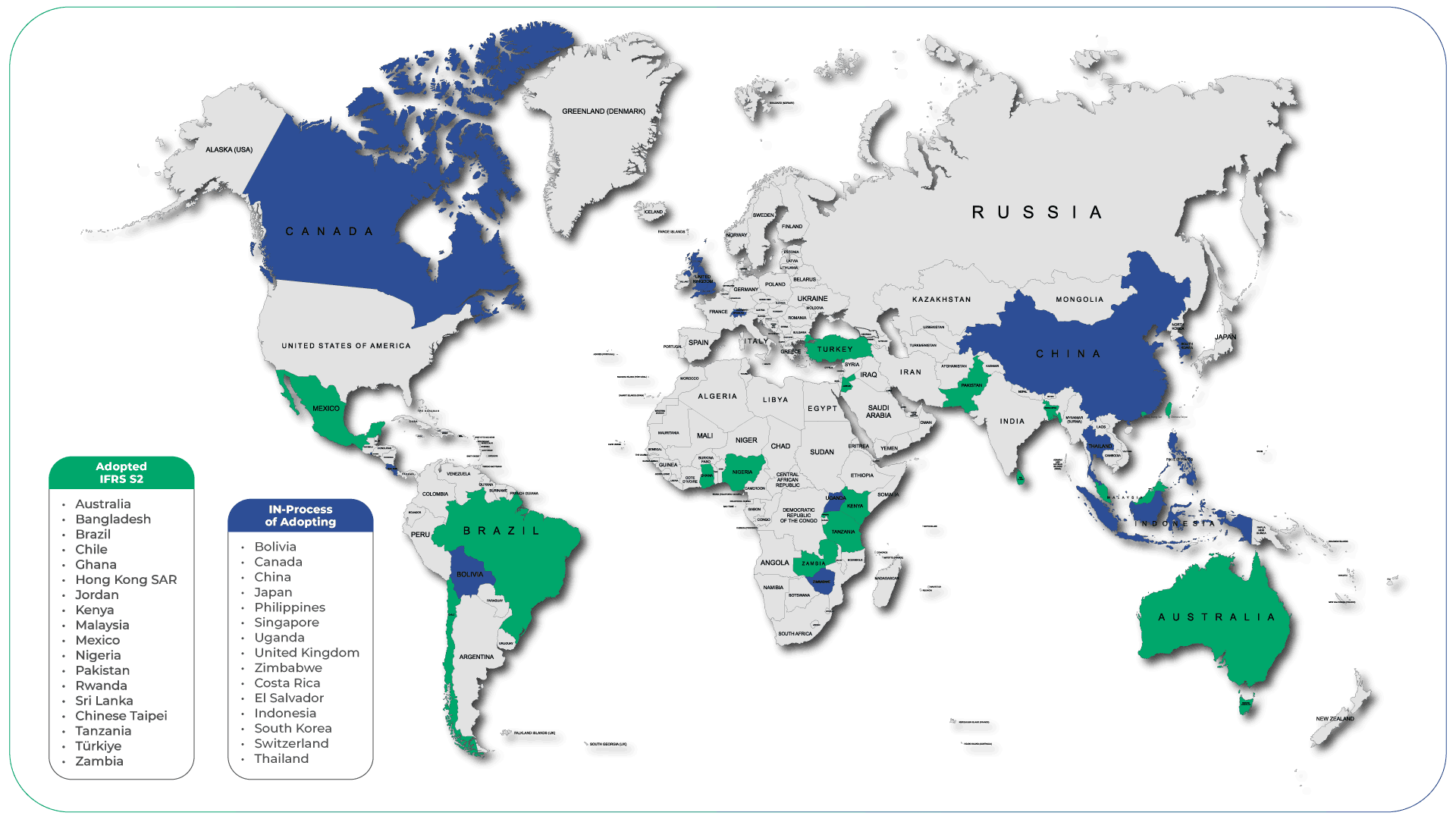

Who Uses IFRS S2 climate disclosure standards?

Many jurisdictions have incorporated or are in the process of incorporating ISSB S2 into their regulatory frameworks and gain significant momentum worldwide, moving quickly towards achieving the global baseline.

Overview of U.S. Climate Disclosure Frameworks

Enhancement and Standardization of Climate-Related Disclosures for Investors of U.S. Securities and Exchange Commission issued for SEC regulated entities.

What is the Objective of SEC Climate Related Disclosures?

The aim is to ensure that investors get the important and relevant information to make informed decisions and highlighting material climate risks that could significantly affect a company’s financial performance.

Are Climate Disclosures Mandatory?

SEC Climate Related Disclosures are mandatary for all the companies registered with the SEC and publicly traded in the U.S. and other entities can voluntarily adopt these standards.

What needs to be disclosed under the SEC Standards?

Entities shall disclose the following information:

- What are the Climate risks likely to materially affect operations or financial condition.

- Process used for identifying, assessing, and managing material climate-related risks.

- How those identified risks influence strategy and business outlook.

- Material expenditures tied to climate risk mitigation or adaptation efforts

- Disclosures regarding transition plans, if any.

- Disclosures regarding use of tools like scenario analysis or internal carbon pricing.

- Scope 1 and Scope 2 emissions metrics.

- Cost incurred to serve extreme weather events.

- Cost incurred on carbon offsets or renewable energy credits.

Disclosures are expected to appear directly in annual reports with a dedicated “Climate-Related Disclosure” section.

What are the Consequences of Non-Disclosure?

Entities may liable to:

- Civil fines of millions of dollars,

- Cease-and-desist orders,

- Legal action if fraud or intentional misstatement is involved.

What is the Major Difference between United States and Global climate disclosure requirements?

Both frameworks encourage the entities toward greater transparency with different priorities:

- IFRS S2 provides a global framework focused on long-term strategy, governance, resilience, and the full emissions picture.

- SEC Standards focus more on financial materiality, ensuring investors understand how climate risks translate into real financial impacts.

Conclusion

Climate related disclosures are rapidly shifting from a voluntary practice to a fundamental requirement for financial stability and market efficiency and these disclosures allow investors to make informed decisions, reduce the cost of capital for sustainable firms, and force organizations to integrate long-term climate resilience into their business strategies. Hence the question is no longer whether companies will report climate risk; rather, how consistently and credibly the companies are doing so across the borders.

Disclaimer

The information provided in this article is intended for general informational purposes only and should not be construed as legal advice. The content of this article is not intended to create and receipt of it does not constitute any relationship. Readers should not act upon this information without seeking professional legal counsel.

Join Our WhatsApp Channel For Global Regulatory Updates & Analysis Join Now